Rebutting the anti-gold propaganda of the mainstream media can be an exhausting process. We see mound after mound of pseudo-analysis claiming that gold should be priced at $1,200/oz (USD), $1,000/oz, or even more ludicrous numbers to the down side. Countering such babble is a two-stage process. First we must address all of the silly arguments which are presented. Then we must construct a separate, additional argument, explaining how/why the price of gold should be at much higher price levels than the inane figures which appear in the mainstream media.

Rebutting the anti-gold propaganda of the mainstream media can be an exhausting process. We see mound after mound of pseudo-analysis claiming that gold should be priced at $1,200/oz (USD), $1,000/oz, or even more ludicrous numbers to the down side. Countering such babble is a two-stage process. First we must address all of the silly arguments which are presented. Then we must construct a separate, additional argument, explaining how/why the price of gold should be at much higher price levels than the inane figures which appear in the mainstream media.

Much less common are the opportunities to address the propaganda in terms such as these:

Why Is Gold Not At $2,000/oz – Macquarie

Here we have a Big Bank supplying the anti-gold propaganda, published by the notorious gold-bashers at Kitco. But now the argument is framed (more or less) in rational terms. Why is gold not at/above $2,000?

Regular readers are aware that $2,000/oz (USD) is, at best, only half of what should be the minimum price for gold, today. However, since $2,000/oz would be a new, nominal high for the price of gold, in the eyes of many people this is a number which represents a fair/rational price. Why is the price of gold not at a fair and rational level? Now we are on equal terms with the propagandists. We no longer need to construct two arguments to their one. We only need to address the lack of substance in the propaganda itself.

They [Macquarie] attributed gold’s relative weakness to a stronger U.S. economy, in the form of a strong dollar and higher yields, as well as a lack of physical demand… [emphasis mine]

The language is oh-so familiar. These are the propaganda machine’s Big Three Anti-Gold Myths:

1) The “strong” U.S. economy, and its Never-Ending Recovery.

2) The Almighty Dollar.

3) “Weak demand” for gold.

Anti-gold Myth #1 is actually a two-part myth. Because the U.S. economy is so strong, so goes the propaganda, the Federal Reserve will “soon” be raising interest rates. Yes, “soon”. For eight years, we have been told day after day, week after week, month after month, that the Fed will be raising – and normalizing – interest rates “soon”. As soon as the U.S. economy is “strong enough”, the rate-hikes would start coming like clockwork.

Supposedly, the U.S. economy has been getting stronger and stronger for nearly eight years. Yet all we have seen from the Federal Reserve during this time is a single baby-step toward the normalization of interest rates (and lots and lots of big talk). How do we reconcile this contradiction?

There is no U.S. recovery. It is all statistical exaggeration and outright lies. The U.S. government lies about inflation, everyone knows this. The fiction-peddlers at the Federal Reserve and inside the U.S. government itself pretend there is “no inflation”, while food and housing costs (in particular) spiral higher at never-before-seen rates. The Liars grossly understate the rate of U.S. inflation.

But when you understate inflation, you overstate GDP — automatically. All GDP numbers are “deflated” by the prevailing rate of inflation, otherwise the so-called GDP number would also be measuring the increase in prices. Understate inflation, and thus under-deflate the GDP estimate, and GDP is overstated, on a percentage-for-percentage basis. The U.S. “Recovery” is nothing more than unreported U.S. inflation.

We can also reveal this fiction by exposing the myth of “millions of new jobs” in the U.S. The U.S. economy has continued to lose jobs. The civilian participation report – the measurement of the total number of Americans with actual jobs – shows there are more than 3 million less Americans with jobs than at the start of the mythical Recovery. No new jobs. No GDP growth. No Recovery. Indeed, the U.S. economy has been losing jobs (on a net basis) faster during the so-called Recovery than during the official “recession”.

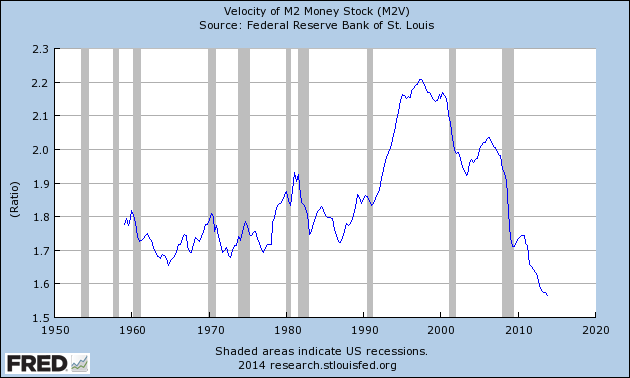

As has been explained before, the velocity of money is analogous to the heartbeat of an economy. Does the chart above show an economy which is “recovering”? No. The all-time lows in this statistical measurement (which is still falling) show an economy which is dying.

As has been explained before, the velocity of money is analogous to the heartbeat of an economy. Does the chart above show an economy which is “recovering”? No. The all-time lows in this statistical measurement (which is still falling) show an economy which is dying.

Anti-gold Myth #2 is even more perverse. The nominal price of gold is not higher, we’re told, because the U.S. dollar is so “strong”. The Bernanke Helicopter Drop alone is an absolute rebuttal of such manure.

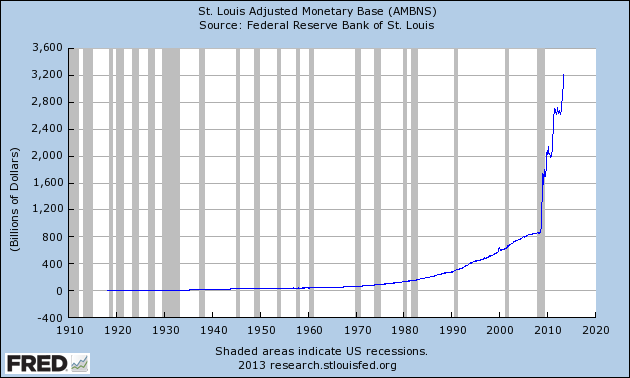

This extreme, out-of-control, exponential function shows a currency which has been hyperinflated, past tense. The U.S. dollar is not “strong”. It is worthless – based upon several, different metrics. Why is the exchange rate of the worthless dollar perched at such an insane level, relative to other paper currencies? Currency manipulation.

This extreme, out-of-control, exponential function shows a currency which has been hyperinflated, past tense. The U.S. dollar is not “strong”. It is worthless – based upon several, different metrics. Why is the exchange rate of the worthless dollar perched at such an insane level, relative to other paper currencies? Currency manipulation.

Don’t take the word of this writer. Go ask the judge who convicted the Big Bank crime syndicate of manipulating all of the world’s currencies, going back to at least 2008. The (worthless) dollar is manipulated higher. The (less-worthless) currencies of other nations are manipulated lower.

This brings us to Anti-gold Myth #3: the price of gold isn’t higher because there just aren’t enough buyers of “physical gold”. The starting point in unraveling this Machiavellian tripe is to point out what the Big Banks and their mouthpieces call “physical gold”: paper.

The Big Banks sell gold “funds” and gold “products” to the hapless Chumps who still choose to do business with them — slips of paper which supposedly represent gold. But there is no gold. Just ask the Chumps who deal with Deutsche Bank. They bought some of its “physical gold”, in the form of that Big Bank’s ultra-fraudulent, bullion-ETF. When some of these Chumps recently asked for delivery of some of their “gold”, they were told that there is no gold – just paper-called-gold.

This fraud has already been out in the open, courtesy of the Big Banks themselves. Informed readers know that India’s government has been pressured (by the bankers) to reduce its gold imports. But the bankers have also suggested how India could reduce its imports of real gold: by selling the Big Bank’s gold “products”.

If India’s consumers still think that they are purchasing the same number of ounces of gold, but actual gold imports to India decline, what does this directly and necessarily imply? It implies that the gold “products” of the Big Banks are not gold, they are paper-called-gold. Indian consumers purchase the same quantities of “gold” but the actual amount of metal backing those purchases declines. Fraud. More banker fraud.

But the perversity increases. At times when the Big Banks are less successful in waylaying Chumps with their assorted paper-gold frauds, we’re told that this means demand for physical gold is “weak”.

Then we have the real world. In the real world; India – the world’s largest gold market — wasn’t pressured to reduce its gold imports because demand was too weak. The government was pressured because (in the eyes of the Big Banks themselves), India’s gold demand was too strong.

Then we have China. China is the world’s other largest gold market. China’s gold-mining industry leads the world in gold production. But China’s government vacuums up every ounce of such gold, and adds it to its own reserves. On top of this; China has been importing somewhere in excess of 1,000 tonnes per year to satisfy the additional demand for real gold amongst its population of 1.3 billion people.

This increasing, relentless demand for gold in China prompted the government to begin open-market purchases of gold last year, internationally, for the first time in at least six years. How much stronger could gold demand in China possibly get?

Meanwhile, the central banks of non-Western, legitimate governments have been accumulating more gold reserves as well, at a rate not seen in more than three decades. More strong demand. And central banks don’t buy their gold by the ounce (or gram). They buy by the tonne.

The Big-Three Anti-gold Myths: not an “ounce” of legitimacy between the three of them (pun intended). Why is gold not at or above $2,000/oz (USD), on the way to much, much higher numbers? The propagandists have no answer to this question, and this is the real “news” in their latest anti-gold propaganda.

Written by Jeff Nelson and published by Bullion Bulls Canada ~ September 6, 2016.

Life, Liberty & All That Jazz is aired at 1:00 p.m. (Eastern Time) for TWO-HOURS, each Monday through Friday on The Micro Effect.

Kettle Moraine, Ltd.

P.O. Box 579

Litchfield Park, AZ 85340

1-623-327-1778

Email: [email protected]

FAIR USE NOTICE: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U. S. C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml

FAIR USE NOTICE: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U. S. C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml