A consultant to GATA (Gold Anti-Trust Action Committee) brought to our attention the fact that gold swaps at the BIS have soared from zero in March 2016 to almost 500 tonnes by August 2017 (GATA – BIS Gold Swaps). The outstanding balance is now higher than it was in 2011, leading up to the violent systematically manipulated take-down of the gold price starting in September 2011 (silver was attacked starting in April 2011).

A consultant to GATA (Gold Anti-Trust Action Committee) brought to our attention the fact that gold swaps at the BIS have soared from zero in March 2016 to almost 500 tonnes by August 2017 (GATA – BIS Gold Swaps). The outstanding balance is now higher than it was in 2011, leading up to the violent systematically manipulated take-down of the gold price starting in September 2011 (silver was attacked starting in April 2011).

The report stimulated my curiosity because most bloggers reference the BIS or articles about the BIS gold market activity without actually perusing through BIS financial statements and the accompanying footnotes. Gold swaps work similarly to Fed repo transactions. When banks need cash liquidity, the Fed extends short term loans to the banks and receives Treasuries as collateral. QE can be seen as a multi-trillion dollar Permanent Repo operation that involved outright money printing.

Similarly, if the bullion banks (HSBC, JP Morgan, Citigroup, Barclays, etc) need access to a supply of gold, the BIS will “swap” gold for cash. This would involve BIS or BIS Central Bank member gold which is loaned out to the banks and the banks deposit cash as collateral to against the gold “loan.” This operation is benignly called a “gold swap.” The purpose would be to alleviate a short term scarcity of gold in London and put gold into the hands of the bullion banks that can be delivered into the eastern hemisphere countries who are importing large quantities of gold (gold swaps outstanding are referenced beginning in 2010).

I wanted dig into the BIS financials and add some evidence from the GATA consultant’s assertions because, since 2009, there has been a curious inverse correlation between the amount of outstanding gold swaps held by the BIS and the price of gold (as the amount of swaps increase, the price of gold declines). You’ll note that in the 2009 BIS Annual Report, there is no reference to gold swaps so we must assume the amount outstanding was zero. By 2011 the amount was 409 tonnes.

The gold swaps enable the BIS to “release” physical gold into the banking system which can then be used to help the Central Banks manipulate the price of gold lower. This explains the jump in BIS gold swaps between March 2016 and March 2017 and the drop in the price of gold from August 2016 until early July 2017. It also explains the rise in the price of gold between July and September this year, which correlates with a decline in the outstanding gold swaps between April and July . Finally, the hit on gold that began earlier this month coincides with a sudden jump in BIS gold swaps in the month of August. (Note: there would be a short time-lag between the gold swap operation and the amount of time it takes to “mobilize” the physical gold)

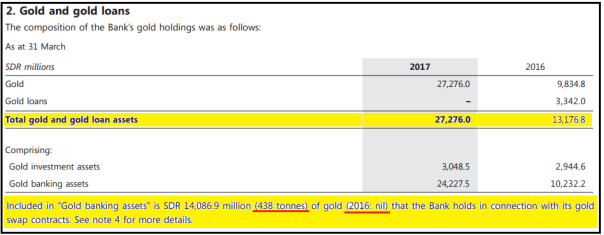

The graphic below shows the increase in gold swaps from March 2016 to March 2017:

As you can see, the total amount of the gold loans outstanding increased by 14.1 billion SDRs (note: the BIS expresses its financials in SDRs). The accompanying note explains that most of this gold loan is comprised of an increase in the BIS’ gold swap contracts outstanding.

As you can see, the total amount of the gold loans outstanding increased by 14.1 billion SDRs (note: the BIS expresses its financials in SDRs). The accompanying note explains that most of this gold loan is comprised of an increase in the BIS’ gold swap contracts outstanding.

I find it interesting that the reports of gold backwardation in London (see James Turk’s interviews on King World News) and the backwardation I have observed between the current-month (delivery month) Comex gold contract and the London gold fixings over the past several months correlates well with the sudden jump in gold swap activity at the BIS.

Backwardation in any commodity market indicates that the demand for delivery of the underlying commodity is greater than the near-term supply of that commodity. It’s hard to ignore that the backwardation observed on the LBMA and with Comex gold delivery-month contracts has been accompanied by soaring gold demand from India, as reported by the Economic Times of India (article link): Gold Imports Jump Three-Fold in April-August.

Furthermore, it appears as if the BIS gold swap activity continued to increase between March 2017 and August 2017, as the BIS’s August Account Statement shows another 2.2 billion SDR increase in amount of outstanding gold loans (a BIS monthly account statement only reports the balance sheet with no accompanying disclosure). These loans primarily are swaps, per the disclosure in the 2017 Annual Report.

However, this jump in gold swaps between March and August is somewhat misleading. The outstanding amount of loans declined from 27.2 billion SDRs at the end of March to 24.6 billion SDRs at the end of July. The price of gold rose over 11% between July and early September. By the end of August, the BIS balance sheet shows 29.3 billion SDRs. A jump of 4.7 billion SDRs worth of gold swaps.

It was around April that the World Gold Council began to forecast that India’s gold importation would drop to 95 tonnes per quarter starting in Q2. As it turns out, India imported 248 tonnes of gold in Q2 2017. This number does not include smuggled gold. Please note the curious correlation between the jump in BIS gold swap activity at the end of the summer and the unexpected surge in Indian gold imports.

In my view, there is a direct correlation between this sudden leap in the amount of gold swaps conducted by the BIS between July and August and the price attack on gold that began two weeks ago. The gold swaps provide bullion bar “liquidity” to the bullion banks who can use them to deliver into the rising demand for deliveries from India, China, Turkey, et al. This in turn relieves the strength and size of “bid” on the LBMA for physical gold which in turn makes it easier for the same bullion banks to attack the price of gold on the Comex using paper gold. This explains the current manipulated take-down in the price of gold despite the rising seasonal demand from India and China.

Written for and published by Investment Research Dynamics ~ September 18, 2017.

Life, Liberty & All That Jazz is aired at 1:00 p.m. (Eastern Time) for TWO-HOURS, each Monday through Friday on The Micro Effect.

Kettle Moraine, Ltd.

P.O. Box 579

Litchfield Park, AZ 85340

1-623-327-1778

Email: [email protected]

FAIR USE NOTICE: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U. S. C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml

FAIR USE NOTICE: This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U. S. C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. For more information go to: http://www.law.cornell.edu/uscode/17/107.shtml