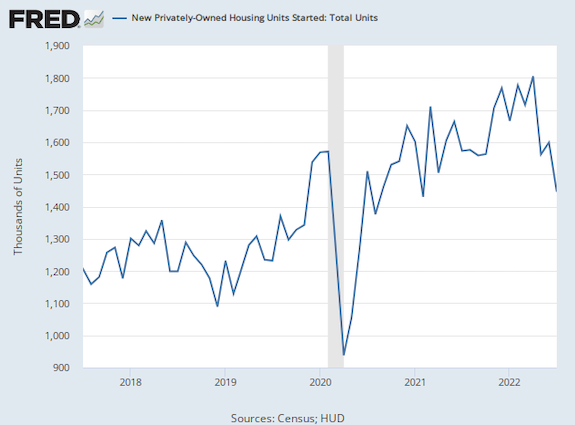

If you are convinced that the economy is already in a recession or hurtling toward one, the housing starts data for July provided more evidence to support your conviction. New housing construction decreased to a seasonally adjusted annualized rate of 1.446 million. This was 9.6 below the June estimate of 1.599 million and 8.1 percent below the year-earlier level. Economists had forecast 1.54 million.

If you are convinced that the economy is already in a recession or hurtling toward one, the housing starts data for July provided more evidence to support your conviction. New housing construction decreased to a seasonally adjusted annualized rate of 1.446 million. This was 9.6 below the June estimate of 1.599 million and 8.1 percent below the year-earlier level. Economists had forecast 1.54 million.

Starts are now down below the prepandemic peak of 1.571 million. The pandemic-induced flight from the cities construction boom peaked in April of this year at 1.805 million. We’re now down nearly 20 percent from that peak.

So it’s fair to call this a bear market for home building. (For the historians out there, the housing bubble peak was 2.273 million in January of 2006, and the all-time high was 2.494 million in January of 1972,)

The decline was even more pronounced in the once blazing single-family market. Construction of new single-family houses fell 10.1 percent to an annual rate of 916,000, below the prepandemic level. Starts have now fallen every month since February 2022. We’re down 24.5 percent since February.

The decline was even more pronounced in the once blazing single-family market. Construction of new single-family houses fell 10.1 percent to an annual rate of 916,000, below the prepandemic level. Starts have now fallen every month since February 2022. We’re down 24.5 percent since February.

“Tighter monetary policy from the Federal Reserve and persistently elevated construction costs have brought on a housing recession,” said National Association of Home Builders chief economist Robert Dietz yesterday when the group’s sentiment survey showed spirits were surprisingly (and now understandably) low.

For those who think the economy is neither in a recession nor on the verge of one, the July industrial production figures provided comfort. The economically sensitive parts of industrial production – manufacturing and mining – pushed the overall production figure up 0.6 percent compared with a month earlier, twice expectations. Capacity utilization bounced to 80.3 percent from June’s 79.9 percent, one-tenth of a point above expectations. Production of the American industrial sector is at an all-time high, eclipsing the previous peak reached in 2018.

Tomorrow’s retail sales numbers will play the role of a tie-breaker. Sales are expected to tick up 0.1 percent. Auto sector production was up 6.6 percent in July, suggesting strong demand. Excluding autos, sales are expected to be down 0.1 percent, largely because gas stations sales likely took a hit from gasoline prices falling every day in the month. Excluding autos and gas, sales are expected to be up 0.3 percent.

If sales do hold up as well as expected, you can be sure some analysts will point out that the economy appears to be more resilient to the Federal Reserve’s hikes than was thought. This makes it sound like news that demand remains strong enough to support surprising growth in industrial production and retail sales. Unfortunately, it’s quite the opposite. It means that the rapid series of rate hikes implemented by the Fed has not cooled off the economy. “Better than expected” figures indicate that the economy has not cooled despite two quarters of negative growth, quantitative tightening, fiscal tightening, and four rate hikes.

The implication for monetary policy is for a lot more tightening from the Federal Reserve than markets current anticipate. If Fed Chairman Jerome Powell is going to bring inflation down to two percent in any reasonable time frame, he will almost certainly have to raise rates enough to decrease demand and raise unemployment. The hotter things stay for longer, the tighter policy will have to get to tame inflation. The good news about last month or the month before that is bad news for months ahead of us.

– Alex Marlow & John Carney

Breitbart News Network

August 16, 2022