Introduction ~ What you are about to read is one of the most interesting commentaries by Murray N. Rothbard that I have been priviledged to read AND to share read – however – what I am posting this evening – is merely an earlier commentary to what would follow some years later – and is ALL a profound bit of history – as relates to economics – including gold and the destruction of economics around the world.

Introduction ~ What you are about to read is one of the most interesting commentaries by Murray N. Rothbard that I have been priviledged to read AND to share read – however – what I am posting this evening – is merely an earlier commentary to what would follow some years later – and is ALL a profound bit of history – as relates to economics – including gold and the destruction of economics around the world.

But what we are publishing – is merely his introduction of the entire story, and was written and published by Rothbard in 1991 and was followed up some years later. Stay tuned my friends – as soon you will have access to the rest of the story. ~ Jeffrey Bennett, Editor

When this essay was published, America was in the midst of the Bretton Woods system, a Keynesian international monetary system that had been foisted upon the world by the United States and British governments in 1945. The Bretton Woods system was an international dollar standard masquerading as a “gold standard,” in order to lend the well-deserved prestige of the world’s oldest and most stable money, gold, to the increasingly inflated and depreciated dollar. But this post-World War II system was only a grotesque parody of a gold standard.

When this essay was published, America was in the midst of the Bretton Woods system, a Keynesian international monetary system that had been foisted upon the world by the United States and British governments in 1945. The Bretton Woods system was an international dollar standard masquerading as a “gold standard,” in order to lend the well-deserved prestige of the world’s oldest and most stable money, gold, to the increasingly inflated and depreciated dollar. But this post-World War II system was only a grotesque parody of a gold standard.

In the pre-World War I “classical” gold standard, every currency unit, be it dollar, pound, franc, or mark, was defined as a certain unit of weight of gold. Thus, the “dollar” was defined as approximately 1/20 of an ounce of gold, while the pound sterling was defined as a little less than 1/4 of a gold ounce, thus fixing the exchange rate between the two (and between all other currencies) at the ratio of their weights.

In the pre-World War I “classical” gold standard, every currency unit, be it dollar, pound, franc, or mark, was defined as a certain unit of weight of gold. Thus, the “dollar” was defined as approximately 1/20 of an ounce of gold, while the pound sterling was defined as a little less than 1/4 of a gold ounce, thus fixing the exchange rate between the two (and between all other currencies) at the ratio of their weights.

Since every national currency was defined as being a certain weight of gold, paper francs or dollars, or bank deposits were redeemable by the issuer, whether government or bank, in that weight of gold. In particular, these government or bank moneys were redeemable on demand in gold coin, so that the general public could use gold in everyday transactions, providing a severe check upon any temptation to over-issue. The pyramiding of paper or bank credit upon gold was therefore subject to severe limits: the ability by currency holders to redeem those liabilities in gold on demand, whether by citizens of that country or by foreigners.

If, in that system, France, for example, inflated the supply of French francs (either in paper or in bank credit), pyramiding more francs on top of gold, the increased money supply and incomes in francs would drive up prices of French goods, making them less competitive in terms of foreign goods increasing French imports and pushing down French exports, with gold flowing out of France to pay for these balance of payments deficits. But the outflow of gold abroad would put increasing pressure upon the already top-heavy French banking system, even more top-heavy now that the dwindling gold base of the inverted money pyramid was forced to support and back up a greater amount of paper francs. Inevitably, facing bankruptcy, the French banking system would have to contract suddenly, driving down French prices and reversing the gold outflow.

If, in that system, France, for example, inflated the supply of French francs (either in paper or in bank credit), pyramiding more francs on top of gold, the increased money supply and incomes in francs would drive up prices of French goods, making them less competitive in terms of foreign goods increasing French imports and pushing down French exports, with gold flowing out of France to pay for these balance of payments deficits. But the outflow of gold abroad would put increasing pressure upon the already top-heavy French banking system, even more top-heavy now that the dwindling gold base of the inverted money pyramid was forced to support and back up a greater amount of paper francs. Inevitably, facing bankruptcy, the French banking system would have to contract suddenly, driving down French prices and reversing the gold outflow.

In this way, while the classical gold standard did not prevent boom-bust cycles caused by inflation of money and bank credit, it at least kept that inflation and those cycles in close check.

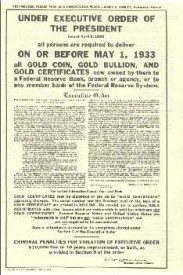

The Bretton Woods system, an elaboration of the British-induced “gold exchange standard” of the 1920s, was very different. The dollar was defined at 1/35 of a gold ounce; the dollar, however, was only redeemable in large bars of gold bullion by foreign governments and central banks. Nowhere was there redeemability in gold coin; indeed, no private individual or firm could redeem in either coin or bullion. In fact, American citizens were prohibited from owning or holding gold at all, at home or abroad, beyond very small amounts permitted to coin collectors, dentists, and for industrial purposes. None of the other countries’ currencies after World War II were either defined or redeemable in gold; instead, they were defined in terms of the dollar, dollars constituting the monetary reserves behind francs, pounds, and marks, and these national money supplies were in turn pyramided on top of dollars.

The Bretton Woods system, an elaboration of the British-induced “gold exchange standard” of the 1920s, was very different. The dollar was defined at 1/35 of a gold ounce; the dollar, however, was only redeemable in large bars of gold bullion by foreign governments and central banks. Nowhere was there redeemability in gold coin; indeed, no private individual or firm could redeem in either coin or bullion. In fact, American citizens were prohibited from owning or holding gold at all, at home or abroad, beyond very small amounts permitted to coin collectors, dentists, and for industrial purposes. None of the other countries’ currencies after World War II were either defined or redeemable in gold; instead, they were defined in terms of the dollar, dollars constituting the monetary reserves behind francs, pounds, and marks, and these national money supplies were in turn pyramided on top of dollars.

The result of this system was a seeming bonanza, during the 1940s and 1950s, for American policymakers. The United States was able to issue more paper and credit dollars, while experiencing only small price increases. For as the supply of dollars increased, and the United States experienced the usual balance of payments deficits of inflating countries, other countries, piling up dollar balances, would not, as before 1914, cash them in for gold. Instead, they would accumulate dollar balances and pyramid more francs, lira, etc. on top of them. Instead of each country, then, inflating its own money on top of gold and being severely limited by other countries demanding that gold, these other countries themselves inflated further on top of their increased supply of dollars. The United States was thereby able to “export inflation” to other countries, limiting its own price increases by imposing them on foreigners.

The Bretton Woods system was hailed by Establishment “macroeconomists” and financial experts as sound, noble, and destined to be eternal. The handful of genuine gold standard advocates were derided as “gold bugs,” cranks and Neanderthals. Even the small gold group was split into two parts: the majority, the Spahr group, discussed in this essay, insisted that the Bretton Woods system was right in one crucial respect: that gold was indeed worth $35 an ounce, and that therefore the United States should return to gold at that rate. Misled by the importance of sticking to fixed definitions, the Spahr group insisted on ignoring the fact that the monetary world had changed drastically since 1933, and that therefore the 1933 definition of the dollar being 1/35 of a gold ounce no longer applied to a nation that had not been on a genuine gold standard since that year.

“Actually, it is difficult to envision in this regard any other criterion, any other standard than Gold. Yes Gold, which does not change in nature, which can be made into either bars, ingots or coins, which as no nationality, which is considered, in all places and all times, the immutable and fiduciary value par excellence.” – Charles de Gaulle

The minority of gold standard advocates during the 1960s were almost all friends and followers of the great Austrian school economist Ludwig von Mises. Mises himself, and such men as Henry Hazlitt, DeGaulle’s major economic adviser Jacques Rueff, and Michael Angelo Heilperin, pointed out that, as the dollar continued to inflate, it had become absurdly undervalued at $35 an ounce. Gold was worth a great deal more in terms of dollars and other currencies, and the United States, declared the Misesians, should return to a genuine gold standard at a realistic, much higher rate. These Austrian economists were ridiculed by all other schools of economists and financial writers for even mentioning that gold might even be worth the absurdly high price of $70 an ounce. The Misesians predicted that the Bretton Woods system would collapse, since relatively hard money countries, recognizing the continuing depreciation of the dollar, would begin to break the informal gentleman’s rules of Bretton Woods and insistently demand redemption in gold that the United States did not possess.

The only other critics of Bretton Woods were the growing wing of Establishment economists, the Friedmanite monetarists. While the monetarists also saw the monetary crises that would be entailed by fixed rates in a world of varying degrees of currency inflation, they were even more scornful of gold than their rivals, the Keynesians. Both groups were committed to a fiat paper standard, but whereas the Keynesians wanted a dollar standard cloaked in a fig-leaf of gold, the monetarists wanted to discard such camouflage, abandon any international money, and simply have national fiat paper moneys freely fluctuating in relation to each other. In short, the Friedmanites were bent on abandoning all the virtues of a world money and reverting to international barter.

Keynesians and Friedmanites alike maintained that the gold bugs were dinosaurs. Whereas Mises and his followers held that gold was giving backing to paper money, both the Keynesian and Friedmanite wings of the Establishment maintained precisely the opposite: that it was sound and solid dollars that were giving value to gold. Gold, both groups asserted, was now worthless as a monetary metal. Cut dollars loose from their artificial connection to gold, they chorused in unison, and we will see that gold will fall to its non-monetary value, then estimated at approximately $6 an ounce.

Keynesians and Friedmanites alike maintained that the gold bugs were dinosaurs. Whereas Mises and his followers held that gold was giving backing to paper money, both the Keynesian and Friedmanite wings of the Establishment maintained precisely the opposite: that it was sound and solid dollars that were giving value to gold. Gold, both groups asserted, was now worthless as a monetary metal. Cut dollars loose from their artificial connection to gold, they chorused in unison, and we will see that gold will fall to its non-monetary value, then estimated at approximately $6 an ounce.

There can be no genuine laboratory experiments in human affairs, but we came as close as we ever will in 1968, and still more definitively in 1971. Here were two firm and opposing sets of predictions: the Misesians, who stated that if the dollar and gold were cut loose, the price of gold in ever-more inflated dollars would zoom upward; and the massed economic Establishment, from Friedman to Samuelson, and even including such ex-Misesians as Fritz Machlup, maintaining that the price of gold would, if cut free, plummet from $35 to $6 an ounce.

The allegedly eternal system of Bretton Woods collapsed in 1968. The gold price kept creeping above $35 an ounce in the free gold markets of London and Zurich; while the Treasury, committed to maintaining the price of gold at $35, increasingly found itself drained of gold to keep the gold price down. Individual Europeans and other foreigners realized that because of this Treasury commitment, the dollar was, for them, in essence redeemable in gold bullion at $35 an ounce. Since they saw that dollars were really worth a lot less and gold a lot more than that, these foreigners kept accelerating that redemption. Finally, in 1968, the United States and other countries agreed to scuttle much of Bretton Woods, and to establish a “two-tier” gold system. The governments and their central banks would keep the $35 redeemability among themselves as before, but they would seal themselves off hermetically from the pesky free gold market, allowing that price to rise or fall as it may.

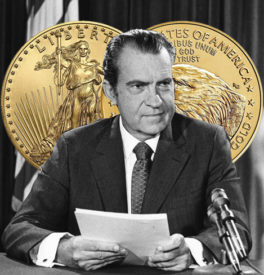

In 1971, however, the rest of the Bretton Woods system collapsed. Increasingly such hard-money countries as West Germany, France, and Switzerland, getting ever more worried about the depreciating dollar, began to break the gentlemen’s rules and insist on redeeming their dollars in gold, as they had a right to do. But as soon as a substantial number of European countries were no longer content to inflate on top of depreciating dollars, and demanded gold instead, the entire system inevitably collapsed. In effect declaring national bankruptcy on August 15, 1971, President Nixon took the United States off the last shred of a gold standard and put an end to Bretton Woods.

In 1971, however, the rest of the Bretton Woods system collapsed. Increasingly such hard-money countries as West Germany, France, and Switzerland, getting ever more worried about the depreciating dollar, began to break the gentlemen’s rules and insist on redeeming their dollars in gold, as they had a right to do. But as soon as a substantial number of European countries were no longer content to inflate on top of depreciating dollars, and demanded gold instead, the entire system inevitably collapsed. In effect declaring national bankruptcy on August 15, 1971, President Nixon took the United States off the last shred of a gold standard and put an end to Bretton Woods.

Gold and the dollar was thus cut loose in two stages. From 1968 to 1971, governments and their central banks maintained the $35 rate among themselves, while allowing a freely-fluctuating private gold market. From 1971 on, even the fiction of $35 was abandoned.

What then of the laboratory experiment? Flouting all the predictions of the economic Establishment, there was no contest as between themselves and the Misesians: not once did the price of gold on the free market fall below $35. Indeed it kept rising steadily, and after 1971 it vaulted upward, far beyond the once seemingly absurdly high price of $70 an ounce. Here was a clear-cut case where the Misesian forecasts were proven gloriously and spectacularly correct, while the Keynesian and Friedmanite predictions proved to be spectacularly wrong. What, it might well be asked, was the reaction of the Establishment, all allegedly devoted to the view that “science is prediction,” and of Milton Friedman, who likes to denounce Austrians for supposedly failing empirical tests? Did he or they, graciously acknowledge their error and hail Mises and his followers for being right? To ask that question is to answer it. To paraphrase Mencken, that sort of thing will happen the Saturday before the Tuesday before the Resurrection Morn.

After a dramatically unsuccessful and short-lived experiment in fixed exchange rates without any international money, the world has subsisted in a monetarist paradise of national fiat currencies since the spring of 1973. The combination of almost two decades of exchange rate volatility, unprecedentedly high rates of peacetime inflation, and the loss of an international money, have disillusioned the economic Establishment, and induced nostalgia for the once-acknowledged failure of Bretton Woods. One would think that the world would tire of careening back and forth between the various disadvantages of fixed exchange rates with paper money, and fluctuating rates with paper money, and return to a classical, or still better, a 100 percent, gold standard. So far, however, there is no sign of a clamor for gold. The only hope for gold on the monetary horizon, short of a runaway inflation in the United States is the search for a convertible currency in the ruined Soviet Union. It may well dawn on the Russians that their now nearly worthless ruble could be rescued by returning to a genuine gold standard, solidly backed by the large Russian stock of the monetary metal. If so, Russia, in the monetary field, might well end up, ironically, pointing to the West the way to a genuine free-market monetary system.

After a dramatically unsuccessful and short-lived experiment in fixed exchange rates without any international money, the world has subsisted in a monetarist paradise of national fiat currencies since the spring of 1973. The combination of almost two decades of exchange rate volatility, unprecedentedly high rates of peacetime inflation, and the loss of an international money, have disillusioned the economic Establishment, and induced nostalgia for the once-acknowledged failure of Bretton Woods. One would think that the world would tire of careening back and forth between the various disadvantages of fixed exchange rates with paper money, and fluctuating rates with paper money, and return to a classical, or still better, a 100 percent, gold standard. So far, however, there is no sign of a clamor for gold. The only hope for gold on the monetary horizon, short of a runaway inflation in the United States is the search for a convertible currency in the ruined Soviet Union. It may well dawn on the Russians that their now nearly worthless ruble could be rescued by returning to a genuine gold standard, solidly backed by the large Russian stock of the monetary metal. If so, Russia, in the monetary field, might well end up, ironically, pointing to the West the way to a genuine free-market monetary system.

![]() Two unquestioned articles of faith had been accepted by the entire economic Establishment in 1962. One was a permanent commitment to paper, and scorn for any talk of a gold standard. The other was the uncritical conviction that the American banking system, saved and bolstered by the structure of deposit insurance imposed by the federal government during the New Deal, was as firm as the rock of Gibraltar. Any hint that the American fractional-reserve banking system might be unsound or even in danger, was considered even more crackpot, and more Neanderthal, than a call for return to the gold standard. Once again, both the Keynesian and the Friedmanite wings of the Establishment were equally enthusiastic in endorsing federal deposit insurance and the FDIC (Federal Deposit Insurance Corporation) despite the supposedly fervent Friedmanite adherence to a market economy, free of controls, subsidies, or guarantees. Those of us who raised the alarm against the dangers of fractional-reserve banking were merely crying in the wilderness.

Two unquestioned articles of faith had been accepted by the entire economic Establishment in 1962. One was a permanent commitment to paper, and scorn for any talk of a gold standard. The other was the uncritical conviction that the American banking system, saved and bolstered by the structure of deposit insurance imposed by the federal government during the New Deal, was as firm as the rock of Gibraltar. Any hint that the American fractional-reserve banking system might be unsound or even in danger, was considered even more crackpot, and more Neanderthal, than a call for return to the gold standard. Once again, both the Keynesian and the Friedmanite wings of the Establishment were equally enthusiastic in endorsing federal deposit insurance and the FDIC (Federal Deposit Insurance Corporation) despite the supposedly fervent Friedmanite adherence to a market economy, free of controls, subsidies, or guarantees. Those of us who raised the alarm against the dangers of fractional-reserve banking were merely crying in the wilderness.

Here again, the landscape has changed drastically in the intervening decades. At first, in the mid-1980s, the fractional-reserve savings and loan banks “insured” by private deposit insurance firms, in Ohio and Maryland, collapsed from massive bank runs. But then, at the end of the 1980s, the entire S&L system went under, necessitating a bailout amounting to hundreds of billions of dollars. The problem was not simply a few banks that had engaged in unsound loans, but runs upon a large part of the S&L system. The result was admitted bankruptcy, and liquidation of the federally operated FSLIC (Federal Savings and Loan Insurance Corporation). FSLIC was precisely to savings and loan banks what the FDIC is to the commercial banking system, and if FSLIC “deposit insurance” can prove to be a hopeless chimera, so too can the long-vaunted FDIC. Indeed, the financial press is filled with stories that the FDIC might well become bankrupt without a further infusion of taxpayer funds. Whereas the “safe” level of FDIC reserves to the deposits it “insures” is alleged to be 1.5 percent, the ratio is now sinking to approximately 0.2 percent, and this is held to be cause for concern.

The important point here is a basic change that has occurred in the psychology of the market and of the public. In contrast to the naive and unquestioning faith of yesteryear, everyone now realizes at least the possibility of collapse of the FDIC. At some point in the possibly near future, perhaps in the next recession and the next spate of bad bank loans, it might dawn upon the public that 1.5 percent is not very safe either, and that no such level can guard against the irresistible holocaust of the bank run. At that point, ignoring the usual mendacious assurances and soothing-syrup of the Establishment, the commercial banks might be plunged into their ultimate crisis. The United States authorities would then be faced with two stark choices.

One would be to allow the entire banking system to collapse, along with virtually all the deposits and depositors in that system. Since, given the mind-set of American politicians, and their evident philosophy of “too big to fail,” it is certain that they would be forced to embrace the second alternative: massive, hyper-inflationary printing of enough cash to pay off all the bank liabilities. The redeposit of such cash in the banking system would bring about an immediate runaway inflation and a massive flight from the dollar.

One would be to allow the entire banking system to collapse, along with virtually all the deposits and depositors in that system. Since, given the mind-set of American politicians, and their evident philosophy of “too big to fail,” it is certain that they would be forced to embrace the second alternative: massive, hyper-inflationary printing of enough cash to pay off all the bank liabilities. The redeposit of such cash in the banking system would bring about an immediate runaway inflation and a massive flight from the dollar.

Such a future scenario, once seemingly unthinkable, is now definitely on the horizon. Perhaps realization of this plight will lead to increased interest, not only in gold, but also in a 100 percent banking system grounded upon a revalued gold stock.

In one sense, 100 percent banking is now easier to establish than it was in 1962. In my original essay, I called upon the banks to start issuing debentures of varying maturities, which could be purchased by the public and serve as productive channels for genuine savings which would neither be fraudulent nor inflationary. Instead of depositors each believing that they have a total, say, of $1 billion of deposits, while they are all laying claim to only $100 million of reserves, money would be saved and loaned to a bank for a definite term, the bank then relending these savings at an interest differential, and repaying the loan when it becomes due. This is what most people wrongly believe the commercial banks are doing now.

Since the 1960s, however, precisely this system has become widespread in the sale of certificates of deposit (CDs). Everyone is now familiar with purchasing CDs, and demand deposits can far more readily be shifted into CDs than they could have three decades ago. Furthermore, the rise of money market mutual funds (MMMF) in the late 1970s has created another readily available and widely used outlet for savings, outside the commercial banking system. These, too, are a means by which savings are being channeled into short-run credit to business, again without creating new money or generating a boom-bust cycle. Institutionally it would now be easier to shift from fractional to 100 percent reserve banking than ever before.

Murray Rothbard

Unfortunately, now that conditions are riper for 100 percent gold than in several decades, there has been a defection in the ranks of many former Misesians. In a curious flight from gold characteristic of all too many economists in the twentieth century, bizarre schemes have proliferated and gained some currency: for everyone to issue his own “standard money”; for a separation of money as a unit of account from media of exchange; for a government-defined commodity index, and on and on.

It is particularly odd that economists who profess to be champions of a free-market economy, should go to such twists and turns to avoid facing the plain fact: that gold, that scarce and valuable market-produced metal, has always been, and will continue to be, by far the best money for human society.

Murray N. Rothbard

Las Vegas, Nevada

September, 1991