“The barbarian hopes — and that is the mark of him, that he can have his cake and eat it too. He will consume what civilization has slowly produced after generations of selection and effort, but he will not be at pains to replace such goods, nor indeed has he a comprehension of the virtue that has brought them into being. We sit by and watch the barbarian. We tolerate him in the long stretches of peace, we are not afraid. We are tickled by his irreverence; his comic inversion of our old certitudes; we laugh. But as we laugh we are watched by large and awful faces from beyond, and on these faces there are no smiles.” ~ Hilaire Belloc, This and That and the Other, 1912

“The barbarian hopes — and that is the mark of him, that he can have his cake and eat it too. He will consume what civilization has slowly produced after generations of selection and effort, but he will not be at pains to replace such goods, nor indeed has he a comprehension of the virtue that has brought them into being. We sit by and watch the barbarian. We tolerate him in the long stretches of peace, we are not afraid. We are tickled by his irreverence; his comic inversion of our old certitudes; we laugh. But as we laugh we are watched by large and awful faces from beyond, and on these faces there are no smiles.” ~ Hilaire Belloc, This and That and the Other, 1912

There is perhaps no greater misunderstanding in modern American life than the widespread belief that the economic system under which we presently live bears a close resemblance to the free-market capitalism envisioned by the architects of classical liberalism. Across the political spectrum, citizens increasingly express dissatisfaction with economic outcomes they attribute to capitalism itself.

They see soaring public debt, endless monetary intervention, politically favored corporations, recurring financial bubbles, widening barriers to entry, regulatory capture, and a financial sector that appears insulated from the consequences of its own mistakes. They observe a government that borrows trillions, spends trillions, guarantees trillions, and increasingly seeks to guide the direction of entire industries. They witness a growing fusion of economic and political power and conclude that they are living through the final excesses of laissez-faire capitalism.

They are mistaken.

In the grand theater of human affairs, where men seek to better their condition through effort and exchange, the economy reveals itself not as a machine to be steered by distant authorities, but as the spontaneous order arising from countless individual choices, each guided by local knowledge and personal incentives. The wise observer looks beyond the immediate spectacle — the flood of liquidity, the towering ledgers of public obligation, the glittering promises of technological deliverance — to the hidden consequences that ripple across generations. What appears as salvation through intervention often masks the quiet erosion of capital, the misdirection of resources, and the subtle theft from the productive by those who wield the coercive power of the state.

In the grand theater of human affairs, where men seek to better their condition through effort and exchange, the economy reveals itself not as a machine to be steered by distant authorities, but as the spontaneous order arising from countless individual choices, each guided by local knowledge and personal incentives. The wise observer looks beyond the immediate spectacle — the flood of liquidity, the towering ledgers of public obligation, the glittering promises of technological deliverance — to the hidden consequences that ripple across generations. What appears as salvation through intervention often masks the quiet erosion of capital, the misdirection of resources, and the subtle theft from the productive by those who wield the coercive power of the state.

Today’s American economy stands at such a juncture, its trajectory shaped by decades of monetary manipulation, fiscal incontinence, and the crony alliances that masquerade as enterprise. Absent a return to the principles of voluntary cooperation, secure property, and restrained governance, the path leads not to abundance but to stagnation, diminished liberty, and the eventual reckoning where illusions collide with arithmetic reality. By 2035, the outlines of this future are discernible: heavier burdens on the industrious, fragile growth shadowed by debt service, and innovation’s promise clouded by political favoritism — unless reason reasserts itself.

What Americans increasingly dislike is not capitalism but its corruption. The system emerging before our eyes is not one of free exchange, private risk, voluntary association, and genuine competition. Rather, it is a system in which political influence determines economic outcomes with increasing frequency; in which losses are socialized while gains remain private; in which market discipline is suspended whenever powerful interests face genuine peril; and in which government intervention has become so commonplace that entire sectors now operate under the assumption that failure itself has become politically unacceptable.

The years following the financial crisis of 2008 accelerated this transformation. The years following the extraordinary interventions of 2020 dramatically expanded it. Together, these events did not create America’s present economic condition, but they reinforced and institutionalized tendencies that had been developing for decades.

The years following the financial crisis of 2008 accelerated this transformation. The years following the extraordinary interventions of 2020 dramatically expanded it. Together, these events did not create America’s present economic condition, but they reinforced and institutionalized tendencies that had been developing for decades.

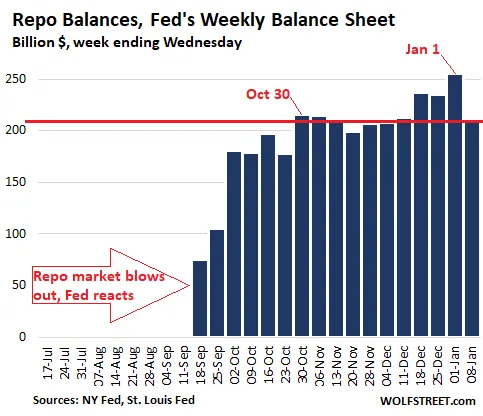

Consider first the monetary realm, where the visible hand of central authority has long supplanted the discipline of genuine markets. In the years preceding and following the disruptions of 2008, and again with the strains evident from late 2019 into 2020, authorities flooded the system with credit. Repo markets signaled distress as overnight rates spiked, prompting injections on a massive scale — tens of billions daily at first, escalating dramatically amid broader panic. Balance sheets swelled, assets were acquired, and the illusion of stability was purchased at the price of future distortion. Such actions do not create wealth; they redistribute claims upon it. By suppressing the true cost of borrowing, they encourage leverage, inflate asset valuations beyond sustainable fundamentals, and sow the seeds of instability. Prolonged periods of apparent calm breed ever-riskier behavior: enterprises and households shift from prudent hedging to speculative positions reliant on continued easy conditions, and ultimately to arrangements that can only persist through perpetual expansion or external rescue. History whispers of similar episodes — manias fueled by credit, followed by panic when confidence falters and insiders exit while others cling to fading hopes.

Consider first the monetary realm, where the visible hand of central authority has long supplanted the discipline of genuine markets. In the years preceding and following the disruptions of 2008, and again with the strains evident from late 2019 into 2020, authorities flooded the system with credit. Repo markets signaled distress as overnight rates spiked, prompting injections on a massive scale — tens of billions daily at first, escalating dramatically amid broader panic. Balance sheets swelled, assets were acquired, and the illusion of stability was purchased at the price of future distortion. Such actions do not create wealth; they redistribute claims upon it. By suppressing the true cost of borrowing, they encourage leverage, inflate asset valuations beyond sustainable fundamentals, and sow the seeds of instability. Prolonged periods of apparent calm breed ever-riskier behavior: enterprises and households shift from prudent hedging to speculative positions reliant on continued easy conditions, and ultimately to arrangements that can only persist through perpetual expansion or external rescue. History whispers of similar episodes — manias fueled by credit, followed by panic when confidence falters and insiders exit while others cling to fading hopes.

The most important consequence of these crises was not the immediate damage they caused. It was the lesson policymakers drew from them. Increasingly, every economic problem came to be viewed through the lens of intervention. Every downturn required stimulus. Every instability required liquidity. Every major institutional failure threatened systemic catastrophe. Every market correction became something to be softened, delayed, or prevented altogether.

The most important consequence of these crises was not the immediate damage they caused. It was the lesson policymakers drew from them. Increasingly, every economic problem came to be viewed through the lens of intervention. Every downturn required stimulus. Every instability required liquidity. Every major institutional failure threatened systemic catastrophe. Every market correction became something to be softened, delayed, or prevented altogether.

Over time, an entire generation of investors, corporations, policymakers, and citizens came to expect government action not merely during emergencies but as a permanent feature of economic life.

This expectation has profound consequences.

The unseen here is profound. Savings lose their signaling power; genuine investment in productive capacity gives way to malinvestment in projects viable only under artificial conditions. The purchasing power of money erodes, punishing those who defer gratification and rewarding debtors, especially the largest one. When authorities later withdraw the punch bowl, as they must to combat the resulting price surges, the adjustment proves painful. Yet the temptation persists: further intervention to ease the very symptoms previously induced. This cycle undermines the moral foundation of contract and responsibility. Men come to expect rescue, banks and corporations internalize the put, and the public bears the diffused costs through inflation or taxation.

A sound system demands transparency in pricing, the possibility of failure to clear errors, and money that holds value as a reliable store and medium. Without it, the economy drifts toward fragility, where each boom plants deeper the roots of the subsequent bust. By the mid-2030s, continued reliance on such tools risks embedding higher baseline inflation, volatile capital flows, and reduced real returns for savers, crowding out the patient accumulation that funds true progress.

Markets derive their value not from perfection but from discipline. They function because prices communicate information, profits reward successful decisions, and losses punish unsuccessful ones. The entrepreneur who misallocates resources suffers consequences. The investor who makes poor judgments bears the cost. The business that fails to satisfy consumers eventually disappears. These processes are not flaws within capitalism. They are the very mechanisms through which capitalism corrects itself.

When government repeatedly intervenes to suppress these signals, however well-intentioned the motive, the result is distortion. Risks that should be recognized become hidden. Investments that should be questioned continue attracting capital. Institutions that should restructure continue operating unchanged. Capital increasingly flows not toward productive enterprise but toward those activities most likely to receive political protection.

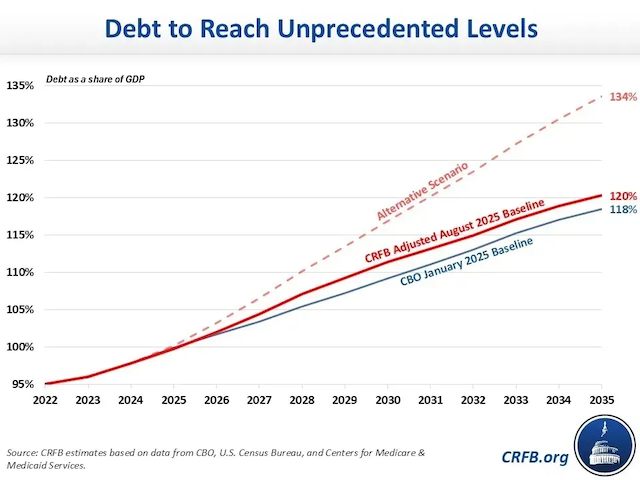

Parallel to this monetary disorder runs the fiscal imbalance, a doomsday mechanism driven by the logic of concentrated benefits and dispersed costs. Gross public obligations have climbed past $39 trillion, with debt held by the public nearing or exceeding 100 percent of annual output in recent assessments. Compare this to earlier epochs, before the apparatus of perpetual war and welfare took root, before income taxes and central banking enabled endless deferral of reckoning. Per capita burdens, adjusted for purchasing power, stand orders of magnitude higher. Population growth accounts for little; the explosion stems from expanding claims — entitlements for retirement and health, defense augmentations, emergency measures, and the political reluctance to trim any sacred stream. Recent years have seen trillions added under varying administrations, each building upon the last in a bipartisan consensus that treats restraint as optional. One administration’s term might accelerate through tax policies or supplemental outlays; another through expansive relief or infrastructure. The continuity lies in the incentives: legislators deliver visible favors today, deferring the bill to tomorrow’s taxpayers and bondholders.

Examine the maturity structure and interest dynamics for clarity. A significant portion of outstanding obligations carries low coupons from eras of repression, now facing rollover at prevailing market rates. Short-term debt turns over quickly, exposing the Treasury to immediate shifts; longer maturities, issued in volume during accommodative phases, harbor larger gaps between legacy yields and current expectations. A weighted average near 3 percent might rise toward 4 percent or higher upon refinancing, adding hundreds of billions annually in carrying costs — even before further rate pressures from persistent deficits or external shocks. Projections indicate net interest surpassing $1 trillion yearly soon, climbing toward $2 trillion by the mid-2030s, consuming an ever-larger share of revenues. On a per-household basis, this translates to thousands of dollars diverted from private use to service yesterday’s promises. Entitlements, driven by aging demographics, compound the pressure; spending drifts toward 27–28 percent of output while revenues hover near 18–19 percent, yielding structural gaps of 6–9 percent absent reform.

Examine the maturity structure and interest dynamics for clarity. A significant portion of outstanding obligations carries low coupons from eras of repression, now facing rollover at prevailing market rates. Short-term debt turns over quickly, exposing the Treasury to immediate shifts; longer maturities, issued in volume during accommodative phases, harbor larger gaps between legacy yields and current expectations. A weighted average near 3 percent might rise toward 4 percent or higher upon refinancing, adding hundreds of billions annually in carrying costs — even before further rate pressures from persistent deficits or external shocks. Projections indicate net interest surpassing $1 trillion yearly soon, climbing toward $2 trillion by the mid-2030s, consuming an ever-larger share of revenues. On a per-household basis, this translates to thousands of dollars diverted from private use to service yesterday’s promises. Entitlements, driven by aging demographics, compound the pressure; spending drifts toward 27–28 percent of output while revenues hover near 18–19 percent, yielding structural gaps of 6–9 percent absent reform.

Still, for the mañana crowd the significance of the per capita debt equivalent at $240,000 should not be gainsaid. If you dial back barely 114 years to 1912 — before America had its Military Industrial Complex, a Welfare State, an income tax or a central bank — the public debt stood at just $2.8 billion!

That’s right. It barely amounted to $30 per capita. Moreover, when you give the money-printers at the Fed, which was created the very next year, their due and adjust the debt figure to inflated 2026 dollars, the public debt in 1912 amounted to just $900 per capita.

And although our national debt is currently just a little over $39 trillion, the amount of that debt held by the public is $31.6 trillion, a real recipe for disaster for our society and nation brewing just over the horizon.

Here the knowledge problem asserts itself. No central authority possesses the dispersed information to allocate such vast resources efficiently or foresee the intricate trade-offs. Politicians face incentives to expand rather than contract, ring-fencing major programs while promising additions. Defense rises with geopolitical tensions; retirement and medical commitments grow with longevity and voter power. Attempts at closure through steeper levies on higher earners founder against reality: those deciles already shoulder the bulk of the load, and further extraction risks deterring the very activity that generates revenue. The result is compounding: deficits beget more debt, which begets higher interest, which enlarges deficits.

By 2035, debt-to-GDP ratios project toward 120 percent or more under baseline assumptions, with adverse scenarios — recession, higher rates, slower growth — pushing far beyond. Real potential output growth, constrained by demographics (slower labor force expansion, aging), hovers around 1.8 percent, insufficient to outpace the arithmetic without painful adjustments.

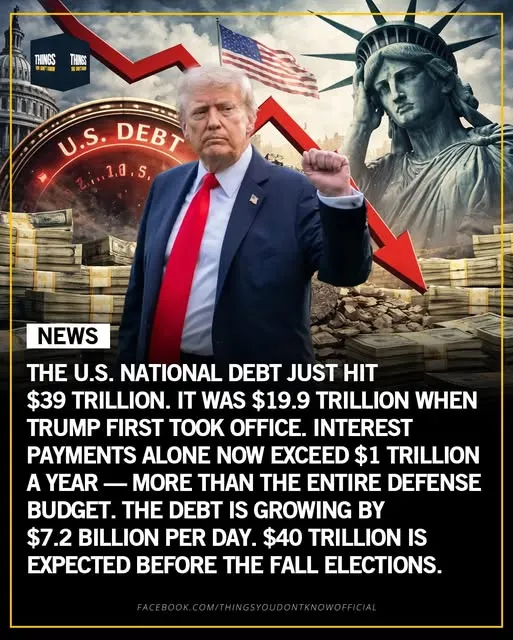

Image: It stood at $19.95 trillion when President Donald Trump took office on January 20th 2017. One must note that nearly $9 trillion of this was added under the Biden regime. So far, over the course of the first Trump term and to this point in his second term, he has overseen the addition of $10.4 trillion to our national debt.

Image: It stood at $19.95 trillion when President Donald Trump took office on January 20th 2017. One must note that nearly $9 trillion of this was added under the Biden regime. So far, over the course of the first Trump term and to this point in his second term, he has overseen the addition of $10.4 trillion to our national debt.

Energy and external events illustrate further unseen linkages. Policies promoting domestic production offer buffers, yet global markets arbitrage prices relentlessly. Geopolitical strains transmit inflation regardless of net export status; strategic reserves provide temporary relief at the cost of future flexibility. “Drill, baby, drill” aligns with abundance through private initiative but cannot repeal scarcity signals or the consequences of disrupted supply chains. When combined with fiscal expansion, it risks amplifying price pressures rather than neutralizing them. The citizen at the pump or the factory floor feels the bite, even as aggregate statistics obscure the localized distortions.

Energy and external events illustrate further unseen linkages. Policies promoting domestic production offer buffers, yet global markets arbitrage prices relentlessly. Geopolitical strains transmit inflation regardless of net export status; strategic reserves provide temporary relief at the cost of future flexibility. “Drill, baby, drill” aligns with abundance through private initiative but cannot repeal scarcity signals or the consequences of disrupted supply chains. When combined with fiscal expansion, it risks amplifying price pressures rather than neutralizing them. The citizen at the pump or the factory floor feels the bite, even as aggregate statistics obscure the localized distortions.

Now turn to the intersection of technology and governance, where cronyism reveals its most seductive face. Recent arrangements in advanced computing exemplify the pattern. Consider structures where a producer partially funds an intermediary vehicle that then acquires its own output in volume, booking revenue while financing loops through layered entities — insurers, annuities, offshore vehicles — with elevated leverage and opaque valuations. Assets lacking liquid markets rely on internal models; rapid obsolescence threatens collateral supporting retiree claims. Such engineering echoes past episodes where complexity veiled risk, bundling promises that unraveled when underlying assumptions failed. Legality shields the forms, yet legitimacy dissolves under scrutiny: retirees unknowingly shoulder speculative exposure, capital flows not according to consumer sovereignty but political connections and narrative momentum.

This is not the organic emergence of value through voluntary exchange but the alliance of ambitious enterprise with state-adjacent power. Discussions of public equity stakes, “strategic” partnerships, or backstops for capital-intensive sectors flow from the same source: firms facing genuine cash burn and uncertain paths to profitability seek stable funding beyond skeptical markets. Valuations propped in private realms falter under public scrutiny and audited reality. Initial public offerings strain as retail participation widens and banks scramble, signaling the hunt for greater fools or ultimate guarantors. When authorities float involvement — framed as national imperative against rivals — it risks transforming innovation into a ward of the treasury. Sunk costs then justify further outlays, transforming error into entrenched subsidy. The unseen includes foregone alternatives: capital directed elsewhere by profit-and-loss discipline, innovations delayed by regulatory overhang, and taxpayer exposure to hype cycles that cool when marginal returns diminish.

Broader still, the public harbors resentment toward “capitalism” that properly belongs to its perversion. Large actors often prefer barriers, preferences, and moats over open competition. Regulation, sold as protection or equity, frequently entrenches incumbents. Historical precedents abound: mandates encouraging unsound lending, guarantees socialized risk, and rating illusions amplified contagion. Bail mechanisms varied in repayment, but the precedent of selective rescue lingers. Today’s variants — structured credit around ephemeral compute, industrial policy cloaked in security — follow suit. The regular everyday ordinary American senses plunder yet misattributes it to markets rather than the fusion of state and favored business, commonly known by educated men as economic fascism. Once government commands sufficient favors to sell, the bidding war intensifies. Democracy’s vulnerability to voting largesse mirrors the market’s to purchased privilege. Neither endures without vigilant defense of principle.

This is accelerated crony statism and fiscal incontinence, not “rapid push into full blown socialism.” Socialism requires state ownership of means of production; here, it’s mixed economy favoritism, regulatory capture, and monetary socialism (fiat expansion). Trump’s AI approach leans pro-innovation with risks of partnership overreach, but the deeper rot predates and transcends one leader. Bipartisan entitlement inertia and spending addiction are the culprits, as both parties still spend worse than drunken sailors.

The consequences rarely appear immediately. Distortion often masquerades as prosperity. Asset prices rise. Credit expands. Consumption increases. Financial markets celebrate. Politicians congratulate themselves. Yet beneath the surface, incentives begin changing in subtle but profound ways.

The history of economic decline rarely begins with poverty. It begins with privilege.

The history of economic decline rarely begins with poverty. It begins with privilege.

This truth was understood by Frederic Bastiat more than a century and a half ago. The gravest threat to liberty was never commerce itself but the tendency of political power to become an instrument through which one group acquires benefits at the expense of another. Whenever government acquires the ability to dispense favors, exemptions, protections, subsidies, guarantees, or special privileges, powerful interests inevitably devote their energies toward securing those benefits. The result is not free enterprise. It is legalized favoritism.

Modern America increasingly exhibits precisely these characteristics.

Large corporations routinely advocate competition in public while seeking protection in practice. Industries that proclaim their faith in markets frequently demand subsidies when conditions become difficult. Financial institutions that celebrate private profit often discover an appreciation for public assistance during moments of crisis. Entire sectors now devote extraordinary resources not toward innovation but toward influencing regulators, legislators, and administrative agencies.

This should surprise no one.

In 1850, writing ‘The Law’, which was a critique of state-sanctioned economic privilege, Frederic Bastiat noted:

“Legal plunder can be committed in an infinite number of ways. Thus we have an infinite number of plans for organizing it: tariffs, protection, benefits, subsidies, encouragements, progressive taxation, public schools, guaranteed jobs, guaranteed profits, minimum wages, a right to relief, a right to the tools of labor, free credit, and so on, and so on. All these plans as a whole – with their common aim of legal plunder – constitute socialism.

But how is this legal plunder to be identified? Quite simply. See if the law takes from some persons what belongs to them, and gives it to other persons to whom it does not belong. See if the law benefits one citizen at the expense of another by doing what the citizen himself cannot do without committing a crime.”

Political economy reinforces the drift. A “uniparty” consensus on sacred spending, augmented by episodic escalations, leaves little room for meaningful retrenchment. Proposals for even modest restraint encounter resistance; voices advocating deeper scrutiny face marginalization. The result is path dependence: expanding commitments, rising baselines, and rhetorical deflection. Trade-offs remain inescapable — more for one claimant means less for producers or future generations. Aging populations intensify the mathematics; slower productivity growth without liberated enterprise compounds it. By 2035, absent course correction, interest alone may rival major discretionary categories, forcing higher taxes, repressed private activity, or monetization that reignites inflation. Growth potential, even augmented by technological diffusion in computation and automation, cannot fully compensate if incentives favor consumption of seed corn over planting. AI holds promise for elevating output per worker, streamlining processes, and unlocking discoveries — but only if markets test and refine applications, not if directed toward politically salient targets. Malinvestment here risks spectacular waste: overbuilt infrastructure, stranded assets, and distorted research agendas.

Political economy reinforces the drift. A “uniparty” consensus on sacred spending, augmented by episodic escalations, leaves little room for meaningful retrenchment. Proposals for even modest restraint encounter resistance; voices advocating deeper scrutiny face marginalization. The result is path dependence: expanding commitments, rising baselines, and rhetorical deflection. Trade-offs remain inescapable — more for one claimant means less for producers or future generations. Aging populations intensify the mathematics; slower productivity growth without liberated enterprise compounds it. By 2035, absent course correction, interest alone may rival major discretionary categories, forcing higher taxes, repressed private activity, or monetization that reignites inflation. Growth potential, even augmented by technological diffusion in computation and automation, cannot fully compensate if incentives favor consumption of seed corn over planting. AI holds promise for elevating output per worker, streamlining processes, and unlocking discoveries — but only if markets test and refine applications, not if directed toward politically salient targets. Malinvestment here risks spectacular waste: overbuilt infrastructure, stranded assets, and distorted research agendas.

Envision the landscape circa 2035 under prevailing tendencies. Public obligations approach or breach levels that test market tolerance, with annual servicing costs extracting resources equivalent to substantial private investment. Entitlements claim growing shares amid retiree expansion. Real growth averages below 2 percent, buffeted by demographics and policy uncertainty. Inflation lingers episodically above comfort, eroding fixed claims and complicating planning. Innovation proceeds unevenly: genuine breakthroughs in energy, biology, and information diffuse where property rights hold, yet crony sectors exhibit boom-bust volatility. Energy independence mitigates some shocks but exposes others through global integration. The middle classes feel squeezed — higher effective burdens, diminished real wages in stagnant pockets, and uncertainty over retirement vehicles exposed to layered risks. Liberty contracts as dependency deepens; the sphere of voluntary action shrinks before administrative decree and fiscal necessity.

When government possesses the power to shape markets, markets will devote increasing effort toward shaping government.

The relationship becomes symbiotic.

Politicians seek economic allies capable of advancing policy objectives. Corporations seek political allies capable of advancing commercial objectives. Each strengthens the other. The public pays the bill.

Politicians seek economic allies capable of advancing policy objectives. Corporations seek political allies capable of advancing commercial objectives. Each strengthens the other. The public pays the bill.

The resulting system differs significantly from traditional socialism. Under socialism, the state owns productive assets directly. Under the emerging American model, ownership remains nominally private. Factories remain privately held. Corporations remain publicly traded. Entrepreneurs continue operating businesses.

Yet increasingly, the boundaries of economic activity are shaped by political calculation.

Investment decisions become influenced by anticipated subsidies. Energy markets become influenced by regulatory mandates. Financial markets become influenced by central-bank expectations. Technology industries become influenced by government contracts, strategic initiatives, and policy preferences. Healthcare operates through layers of public reimbursement and regulation. Education increasingly depends upon federal financing. Housing markets remain heavily affected by government-backed credit.

Ownership remains private.

Direction becomes political.

This distinction is critical because it explains why many Americans sense that something fundamental has changed even while conventional measures of capitalism remain intact.

What they are witnessing is not socialism but corporatism.

The danger of corporatism lies not merely in inefficiency. Its deeper danger is moral. It gradually transforms the relationship between success and merit. In a genuinely competitive system, prosperity depends primarily upon creating value for others. In a corporatist system, prosperity increasingly depends upon proximity to political power.

The entrepreneur becomes less important than the lobbyist.

The inventor becomes less important than the regulator.

The consumer becomes less important than the policymaker.

Over time, the culture itself begins changing. Ambition shifts away from productive achievement and toward political influence. Businesses devote resources toward securing favors rather than satisfying customers. Citizens begin viewing government not as a neutral protector of rights but as a source of benefits to be captured.

A free society slowly becomes a competitive scramble for access to public power.

This transformation is visible most clearly in America’s fiscal condition.

The federal debt has reached levels once considered unimaginable. Yet the sheer magnitude of the numbers often obscures the underlying issue. The problem is not merely that the government owes trillions of dollars. The problem is that the political system has largely lost the ability to impose meaningful restraint upon itself.

Every major constituency possesses claims upon the Treasury.

Every program develops defenders.

Every subsidy acquires beneficiaries.

Every expenditure becomes politically necessary.

Meanwhile, the costs remain dispersed across future taxpayers, future borrowers, and future generations.

The result is a government increasingly incapable of saying no.

For decades, debt remained manageable because interest rates remained extraordinarily low. Policymakers came to view this condition almost as a law of nature. Yet low rates were themselves partly a product of unprecedented monetary intervention. They encouraged borrowing, discouraged saving, inflated asset prices, and masked the true cost of government expansion.

As long as money remained inexpensive, fiscal irresponsibility appeared sustainable.

That illusion is fading.

Interest costs now consume an ever-growing share of federal expenditures. Demographic realities place mounting pressure upon entitlement programs. Healthcare obligations continue expanding. Defense commitments remain substantial. Political appetite for spending shows little sign of diminishing.

Ayn Rand, a noted political analyst and author of the 1940s through 1950s era, would most likely denounce America’s current economic system as the antithesis of capitalism: the alliance of businessmen and bureaucrats against the productive.

Real capitalism doesn’t exist without getting rid of the funny money. Therein lies ninety percent of our problems, fiat dollars aka funny money. Stop using funny money and actually back the U.S. currency with something sound again; stop all subsidies to all corporations, no exceptions; end government grants and for God’s sake, for the sake of all Americans stop with all the massive out-of-control spending. Make all citizens earn every dollar by way of whatever skill set they hold. And audit the Federal Reserve, close it down and get America back to using honest money for a change.

Real capitalism doesn’t exist without getting rid of the funny money. Therein lies ninety percent of our problems, fiat dollars aka funny money. Stop using funny money and actually back the U.S. currency with something sound again; stop all subsidies to all corporations, no exceptions; end government grants and for God’s sake, for the sake of all Americans stop with all the massive out-of-control spending. Make all citizens earn every dollar by way of whatever skill set they hold. And audit the Federal Reserve, close it down and get America back to using honest money for a change.

To top it all off, many so-called experts are stating that a massive Artificial Intelligence industry bubble is now very near the point of a catastrophic burst, while some simply think it’s only recalibrating. But most of them are in agreement that this is the one trigger that could set off a more expansive and destructive economic collapse when it occurs. The question isn’t if it will collapse but when the collapse is coming. While the underlying technology is genuinely transformative, the current financial structure and stock market valuations surrounding it show classic signs of an inflating bubble on the verge of bursting.

At the heart of the AI bubble debate is a colossal disparity between how much money is being spent on infrastructure and how much revenue the technology is actually generating. Tech giants like Amazon, Alphabet, Meta, and Microsoft are pouring staggering amounts of capital into AI infrastructure. J.P. Morgan analysts project roughly $5 trillion will be spent on AI-related infrastructure by 2030. Sequoia Capital estimates that the AI industry needs to make roughly $600 billion a year to justify the massive hardware and data center spending, but annualized revenues for major players like OpenAI and Anthropic are currently a fraction of that.

At the heart of the AI bubble debate is a colossal disparity between how much money is being spent on infrastructure and how much revenue the technology is actually generating. Tech giants like Amazon, Alphabet, Meta, and Microsoft are pouring staggering amounts of capital into AI infrastructure. J.P. Morgan analysts project roughly $5 trillion will be spent on AI-related infrastructure by 2030. Sequoia Capital estimates that the AI industry needs to make roughly $600 billion a year to justify the massive hardware and data center spending, but annualized revenues for major players like OpenAI and Anthropic are currently a fraction of that.

Freedom has always required responsibility. Markets require accountability. Prosperity requires production. Wealth must ultimately be created before it can be held in the hands of those who rightly earned it, to keep for themselves or willingly redistribute a portion to charities or have the government steal for its welfare programs.

No nation, regardless of its power or resources, can permanently evade these realities.

America enters the decade ahead possessing extraordinary strengths. Its entrepreneurial culture remains vibrant. Its technological leadership remains significant. Its capital markets remain among the deepest in the world. Its citizens continue demonstrating remarkable ingenuity and resilience.

Predictions of imminent collapse could be off base, dependent on what future course America and Her leaders take the country. We will all find out together soon enough, I suspect.

The choice resides in understanding consequences. When law organizes spoliation — disguised as necessity, equity, or strategy — society consumes its capital while pretending abundance. When producers retain the product of their minds and hands, civilization ascends. The American experiment, rooted in recognition of individual rights and limited powers, demonstrates the latter’s potency. Recovery demands discarding the fallacy that authority can conjure prosperity without cost, embracing instead the discipline that aligns action with reality. Fiscal temperance, monetary soundness, and separation of state from market favoritism form the pillars.

By 2035, America may yet stand as beacon of opportunity, its economy vibrant through the liberated mind — or bear the accumulated weight of deferred reckonings. The trajectory depends on reclaiming sight of the unseen: that true wealth flows from creation, not commandeering; from liberty, not license. Reason, effort, and moral clarity remain the surest guides.

The fundamental issue is whether economic outcomes will continue to be determined primarily by voluntary exchange or increasingly by political allocation.

Every society must ultimately choose between these paths.

One trusts individuals.

The other trusts institutions.

One disperses power.

The other concentrates it.

One accepts failure as the price of progress.

The other attempts to eliminate failure and ultimately undermines progress itself.

The American experiment has always rested upon the conviction that free people, operating within a framework of law, property rights, and voluntary exchange, can accomplish more than any collection of planners, regulators, or administrators. That conviction produced the most dynamic economy in human history. It transformed a continental republic into a global power. It elevated living standards beyond the imagination of previous generations.

The question before us is whether we still possess sufficient confidence in those principles to preserve them.

For if current trends continue unchecked, America will not awaken in 2035 to find itself transformed into a socialist state. The reality will be subtler and perhaps more troubling. It will find itself governed by an increasingly intricate partnership between political power and economic privilege, sustained by debt, lubricated by monetary intervention, justified by perpetual emergency, and defended by those who profit from its continuation.

Such a system can endure for years.

Perhaps even decades.

But it cannot indefinitely generate the prosperity, innovation, independence, and liberty that arise only from genuinely free men and women operating within genuinely free markets.

And that, more than any recession, financial panic, or political controversy, is the true challenge confronting America’s future.

June 10, 2026

Justin O. Smith ~ Author

~ the Author ~

Justin O. Smith Has Lived in Tennessee Off and on Most of His Adult Life, and Graduated From Middle Tennessee State University in 1980, With a B.S. And a Double Major in International Relations and Cultural Geography – Minors in Military Science and English, for What Its Worth. His Real Education Started From That Point on. Smith Is a Frequent Contributor to the Family of Kettle Moraine Publications.